Before deciding on which form to use, confirm the legal status of the property as a condo, or as a wholly owned individual property. Although not common, there are some single family developments which are deeded as condos. There are also many half-duplexes which are not condos.

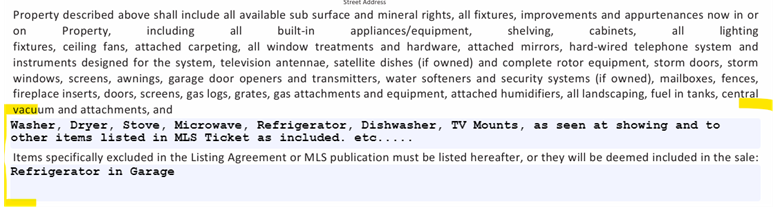

Inclusions: Remember that items listed as inclusions in an MLS listing have no legal effect unless they are specifically included in an Offer to Purchase. Inclusions should include everything the buyer is expecting, or wants, to be included in the sale. Appliances including oven/range, refrigerator, microwave, dishwasher, disposal, washer, dryer, water softener (if not rented), security system hardware, invisible fencing, play structures, whole house or surround sound audio equipment, snow blower, lawn mower, satellite dish, TV mounts, are all examples of possible inclusions.

Items not included: “Seller’s personal property”, plus anything noted as being excluded in the MLS listing, as well as any rented equipment (security system, water softener, filter, satellite dish)

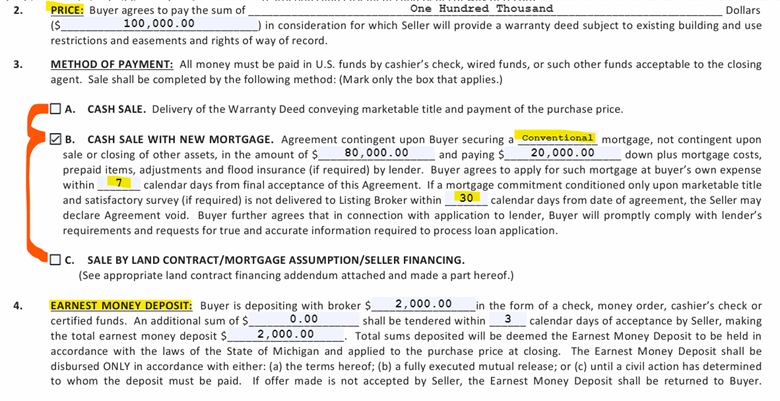

Price: What is the offering price, input into the appropriate section.

Financing contingency: Having a detailed pre-approval letter will be helpful when completing the financing contingency. We need to know the type of loan (conventional, FHA/VA), and we may need to confirm with the lender the time to close. This contingency, like all others, cannot be changed after an offer is accepted, unless the seller agrees to it.

Earnest money: Typically 1% or more of offer price, discuss with your client.

Delivery of Documents: No need to complete any option other than “Email”.

Closing: Should allow a minimum of 30 days if purchase is financed. If lender is unknown to you or from out of state, you may want to use 35 or 40 days. Cash closings can be done in 2-3 weeks pending an appraisal. Discuss with your client.